Listen to the podcast:

Making Aliyah is exciting, but the money side can get stressful fast: opening a bank account, funding your first months in Israel, and converting foreign currency without losing a hidden percentage along the way. This guide is written for new olim (new immigrants to Israel; oleh in singular) who want a clear plan and practical guardrails.

Nothing here is personal financial or tax advice. Use it to ask better questions, compare options, and avoid the most common (and expensive) mistakes.

What are the three money decisions you should make before you land in Israel?

Before your flight, decide (1) how you will access shekels in your first week, (2) how you will transfer larger amounts once you have an Israeli account, and (3) which documents will prove where your money came from. If you make these choices early, you avoid panic conversions at terrible rates and “compliance freezes” later.

Which documents should you pack so banks don’t block your transfers later?

Bring a “source-of-funds” folder that explains your money in plain English: bank statements, pay slips, pension statements, a home sale contract, or an inheritance letter. Israeli banks are required to ask, especially for larger transfers, and having documents ready turns a scary call into a quick email. Pack digital copies plus paper backups.

- Identity: passport, Israeli ID (Teudat Zehut) if you already have it, and your immigrant certificate (Teudat Oleh) once issued.

- Address: a lease, utility bill, or a signed letter from a host plus their proof of address if you are staying with family.

- Source of funds: recent statements and a short one-page explanation (example template later in this guide).

- Tax ID: if you are a U.S. citizen, bring your SSN and be ready for FATCA questions (FATCA is a U.S. law that makes foreign banks report certain accounts).

“Source of funds” note generator

How much cash should you bring, and when do you need to declare it?

Carry enough for a week of basics, not your life savings. Cash is useful for taxis, a SIM card, and the first grocery run, but large cash deposits and exchanges get extra scrutiny and often worse pricing. If you enter or leave Israel with cash and equivalents above the legal threshold, you must file a customs report. Government of Israel

At the time of writing, the reporting threshold is ₪50,000 when entering or leaving Israel by air or sea, and ₪12,000 when crossing a land border. The duty is to report, not to pay a tax, but you should follow the form requirements. Government of Israel

A practical target is 1–2 weeks of expenses in shekels, plus a backup card. If you need more liquidity, plan an electronic transfer rather than carrying large sums.

Which accounts should you keep open abroad, and why?

Keep one primary home-country account open for at least 6 months. It covers timing gaps: delayed Israeli card approvals, a transfer that arrives in dollars before conversion, or a bank that needs extra documents. It also lets you pay leftover bills abroad while your Israeli setup stabilizes.

What is the Bank of Israel “representative rate” (shaar yatzig), and why should you check it first?

The Bank of Israel publishes a daily “representative” exchange rate (often called shaar yatzig) that acts as a public benchmark for the shekel against major currencies. It is not the exact rate you will receive, but it helps you estimate what a fair deal looks like and spot bad spreads or misleading “no commission” offers. Bank of Israel

Here is the key vocabulary, defined once so the rest of the guide stays simple:

- Mid-market rate: the midpoint between global buy and sell prices at a given moment.

- Spread: the gap between what a provider buys at and sells at; this gap is a hidden fee.

- Commission/fee: an explicit charge (for example, ₪25 for a conversion), sometimes layered on top of a spread.

Which exchange method usually gives new olim the best all-in rate?

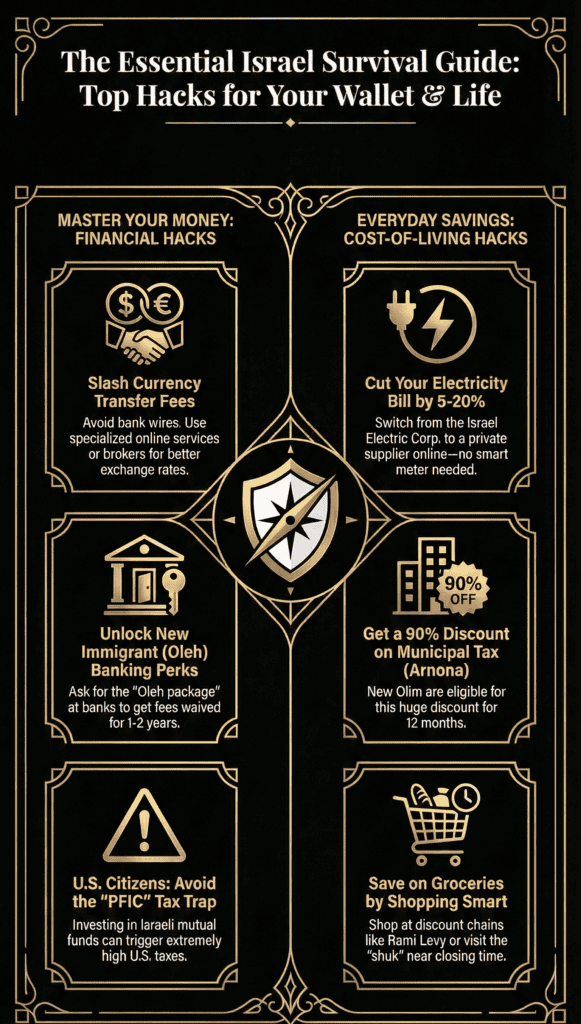

Most new olim save money by splitting the job: use a good card or ATM for small, immediate cash needs, then use a transparent transfer service or licensed FX dealer for larger conversions. Banks can compete only if you negotiate the FX rate and reduce fees. Always compare the total cost.

A quick warning that saves people real money: airport and hotel exchange counters are usually priced for convenience, not fairness. If you must arrive with shekels the same day, use an ATM for a small amount and do the “real” conversion later when you can compare rates.

When should you use a licensed money changer instead of a bank?

Use a licensed money changer when you are converting physical cash and you can compare quotes on the spot. They may advertise “no commission,” but you still pay through the spread, so compare the offered rate to the Bank of Israel benchmark. For one-off cash conversions, changers are often cheaper than bank tellers.

Safety rule: use dealers that are properly licensed and operate transparently, especially for large sums. Israel regulates money service businesses, including foreign currency exchange and money transmission. Government of Israel

Quick quote script (money changer or bank):

- “If I exchange [amount] today in one transaction, what exact rate will I receive in ₪?”

- “Is there any fixed fee on top of that rate?”

- “Can you improve the rate if I do it all at once instead of in smaller conversions?”

When do ATMs and card payments beat cash exchange?

ATMs and card purchases are ideal for your first days because they give instant shekels at a card-network rate. The deal turns bad when your bank adds a foreign transaction fee, an ATM fee, or when the ATM offers to convert into your home currency. Always choose to be charged in shekels.

A good rule: if your total fee is under about 1%, ATMs are hard to beat for convenience. If it is 3% plus fees, it is usually a temporary bridge, not a long-term strategy.

How do you spot a “zero commission” trap in 30 seconds?

Ignore the word “commission” and compare rates. Ask: “What exact exchange rate will I receive right now?” Then compare that number to the Bank of Israel benchmark. The percentage gap is your real fee, even if the receipt says 0. Multiply the gap by your amount to estimate the cost.

Here is a simple method you can do on your phone:

-

Find the benchmark rate.

Use the Bank of Israel representative rate as a reference: Bank of Israel exchange rates -

Compute hidden cost:

hidden cost = amount × benchmark rate × (spread %) -

Add any fixed fees:

bank conversion fee, ATM fee, wire fee

Example calculation (you can copy this):

- Amount: $10,000

- Benchmark: ₪3.20 per $1

- Offered rate is 1.2% worse (spread = 0.012)

- Hidden cost ≈ 10,000 × 3.20 × 0.012 = ₪384

That ₪384 is the “zero commission” you just paid.

Break-even calculator: when does a negotiated bank deal beat a fintech fee?

If you have two options:

- Option A (bank): bank spread % plus a fixed fee (often in ₪)

- Option B (fintech): one all-in fee %

A rough break-even amount in foreign currency is:

break-even ≈ fixed_fee_₪ ÷ (benchmark_rate × (fintech_fee% − bank_spread%))

Example (using round numbers): if the fixed fee is ₪25, the benchmark is ₪3.20 per $1, the fintech fee is 0.7%, and you negotiate the bank spread down to 0.4%:

break-even ≈ 25 ÷ (3.20 × (0.007 − 0.004)) ≈ $2,600

Above that, the bank can be cheaper in theory, but only if the negotiated rate is real and the bank does not add extra charges.

Advanced note for very large conversions

If you are converting a six-figure amount, the “best” option can flip. A bank that gives you a genuinely improved FX rate (and a flat incoming-wire fee) can sometimes beat a fintech’s percentage fee, and an FX specialist may beat both. The non-negotiable rule is to compare net shekels delivered, not marketing claims.

How do you open an Israeli bank account as an oleh without surprises?

Open the account early, pick a branch that actually deals with new immigrants, and treat the first meeting like onboarding, not a transaction. Israeli banks must follow strict anti-money-laundering rules, so the easiest path is to arrive with clean documents, clear answers, and realistic expectations about credit cards and transfers. The goal is a functional account first, perks second.

How to choose a bank (and branch) without overthinking it

- Pick a branch that regularly serves English speakers and new immigrants; the branch culture matters as much as the brand.

- Compare three things in writing: monthly account plan, international transfer fees, and FX conversion policy.

- Ask how quickly you can get a debit card, and what is required to approve a credit card.

If you want a starting shortlist, many olim begin by comparing the big retail banks (Bank Leumi, Bank Hapoalim, Israel Discount Bank, Mizrahi-Tefahot, and First International Bank). Your best choice is the one that gives you the best fee plan plus a branch that answers emails.

What documents and answers do banks expect for compliance?

Expect questions in three buckets: who you are, where you live, and where your money comes from. If you answer these cleanly, everything else moves faster. Prepare to show IDs, proof of address, and the story of your funds (salary, savings, pension, property sale). Large deposits and transfers can trigger extra questions and reporting thresholds.

A practical “answer sheet” to draft in advance:

- Why are you opening the account (salary, benefits, rent, bills)?

- What is your expected monthly inflow/outflow range?

- What is the source of your initial deposit and future transfers?

One useful mental model: banks care less about you and more about documenting the transaction. Large cash activity is especially sensitive. For example, Israeli banks note reporting and documentation duties around cash deposits/withdrawals or currency exchange valued at ₪50,000 or more, under anti-money-laundering rules. Discount Bank

Which account settings prevent avoidable fees in year one?

Choose simplicity: a shekel (ILS) account for day-to-day life, plus a foreign-currency sub-account only if you truly need to hold dollars or euros for a specific purpose. Ask about “package” pricing (a monthly bundle that includes common actions) versus per-transaction fees, and switch as your usage stabilizes. Also ask about discounted “oleh benefits” and when they expire.

One negotiating tip that works: banks often have room to improve your FX rate for a large conversion. Even a 0.5% improvement matters at scale, and it costs you nothing to ask.

Two fee-reduction moves that are often overlooked

- Ask your bank to switch you to the right fee plan for your usage (bundled packages can be cheaper than per-action pricing).

- Do more actions in digital self-service rather than at a teller, since teller actions often cost more.

The Bank of Israel publishes public guidance on lowering account-management and card costs. Bank of Israel

How do you get a debit card, credit card, and Israeli payment tools working fast?

You will usually get a debit card first; credit cards often require income history, a guarantor, or time. If you need one quickly, ask about secured cards, adding a working spouse, or keeping a small regular deposit to build activity. For everyday transfers, set up local tools early, like bank transfers and common payment apps.

What is the smartest way to transfer money from abroad to Israel?

The smartest transfer is the one that survives compliance checks, minimizes all-in cost, and lands as usable shekels when you need them. For large sums, a traditional international wire can still be the most reliable rail, but you must budget for multiple fees and the bank’s conversion spread. For smaller or recurring transfers, transparent fintech pricing can win.

What does a SWIFT wire really cost once you include every layer?

A SWIFT wire is reliable for large sums, but the true cost is a stack: sending fee, possible intermediary deductions, Israeli receiving fee, and the bank’s FX spread when you convert to shekels. Even a small spread can cost more than all fixed fees combined, so estimate the spread cost before you send.

One published rule of thumb is that the Israeli receiving fee can be around 0.33% of the transaction unless you negotiate a flat fee, depending on the bank and route. Nefesh B’Nefesh

A clean way to estimate total cost is:

Total cost ≈ send fee + receive fee + (amount × FX spread)

If your bank spread is 1.5% on a $50,000 transfer, the spread alone can dwarf every fixed fee.

When do services like Wise or Revolut make sense, and what is “Masav”?

These services can win when you want an upfront fee and a rate close to mid-market, especially for recurring or mid-sized transfers. “Masav” is Israel’s domestic bank transfer system; if money lands as a local transfer, some costs can be lower than a full international wire. Always compare a live quote to your bank’s net shekel result.

How do you avoid transfer freezes and source-of-funds drama?

Assume any large inbound transfer will be reviewed. Tell your Israeli bank what is coming, from where, and why, before you send it. Keep a ready packet: statements, sale or pension documents, and a one-page explanation. Send consistent amounts and explanations so you do not look like you are breaking transfers up to dodge reporting.

Also avoid a common mistake: sending shekels from abroad at a bad retail rate. It is often better to send dollars/euros and convert in Israel where you can compare options.

If you are transferring money for a home purchase or other time-sensitive deal, coordinate the transfer plan with whoever is handling the transaction (often your lawyer and the receiving bank branch). FX timing, documentation, and cut-off times can matter as much as the rate when a payment deadline is fixed.

What tax benefits do new immigrants get, and what is changing on January 1, 2026?

Israel offers meaningful tax benefits for new immigrants, especially around foreign-source income, but the details are changing and the paperwork matters. In general, new olim still have a 10-year exemption on foreign-source income, while new disclosure rules beginning January 1, 2026 require more reporting for those who become residents from that date. Government of Israel

Residency-date checkpoint (do not skip this):

- If your Israeli tax residency begins before January 1, 2026: you may fall under the prior reporting regime for the exemption period, but transitional rules can be nuanced.

- If your Israeli tax residency begins on or after January 1, 2026: plan for annual reporting of foreign income and assets even when tax-exempt, unless guidance for your category says otherwise. CWS Israel

What does the 10-year foreign-income benefit cover, and what does it not cover?

The classic “10-year benefit” is an exemption from Israeli tax on foreign-source income for qualifying new immigrants and certain returning residents. Foreign-source usually means the income is generated outside Israel (salary for work performed abroad, foreign dividends, foreign interest). It does not automatically exempt Israeli-source income, and it does not cancel tax obligations you still have in another country. Government of Israel

Define it in your own situation by asking one question: where is the work performed or where is the asset located? That is often what drives “source.”

Will you still have to report foreign income and assets during the holiday?

For residents who begin Israeli tax residency on or after January 1, 2026, published guidance indicates the foreign reporting exemption is being repealed. You may still receive the tax exemption on qualifying foreign-source income, but you can be required to disclose foreign assets and income to the Israeli Tax Authority. Dates matter, so confirm your status. CWS Israel

If you made Aliyah before that date, different transitional rules may apply, so do not guess.

Are there new 2026 incentives on Israeli-source income, and how should you treat the headlines?

There has been public reporting and government communication about a new incentive plan aimed at 2026 arrivals that could temporarily reduce Israeli income tax on Israeli-source earnings up to a capped amount, with rates stepping up over several years. Treat this as “plan-level” information until it is final for your case, and verify eligibility based on your Aliyah date. The Times of Israel

The practical takeaway: do not build a budget around a headline. Build it around confirmed guidance and a conservative estimate.

What should U.S. citizens and other dual taxpayers do differently?

If you still file taxes abroad, Israel’s exemptions do not cancel those obligations. Keep records that let you answer two systems: Israeli residency rules and your home-country reporting. Separate personal and business flows, track the source of each income stream, and get advice early if you have trusts, a company, or large investments.

Which government benefits matter most for your first-year cash flow?

The benefits that matter most are the ones that either put money into your bank account or reduce fixed bills you must pay anyway. For many new olim, that means Sal Klita payments, income tax credit points on Israeli earnings, and time-limited relief on specific costs. Timing is everything, and some benefits require an active Israeli account.

How does the Sal Klita absorption basket get paid, and what pauses it?

Sal Klita is an absorption grant paid in installments to help new immigrants settle, and the amount depends on your household profile. It is typically deposited into your Israeli bank account after you provide details. Official guidance notes that payments can pause if you leave Israel during the eligibility period, then resume when you return. Nefesh B’Nefesh

Action step: open the account early and submit your bank details as soon as you are instructed, so you do not delay the clock.

What other benefits can reduce big expenses in year one?

Beyond Sal Klita, new immigrants can qualify for income tax credit points on Israeli income for a defined period, with the government publishing an official breakdown by months after Aliyah. In addition, some olim receive limited-time relief tied to health system enrollment, and customs benefits can reduce duties on eligible personal goods and, in some cases, vehicles. Government of Israel

Do one thing that saves real money: print your benefits list, write the expiration dates next to each, and set calendar reminders 60 days before each deadline.

Quick view: income tax credit points for new immigrants

Nefesh B’Nefesh summarizes the credit-point schedule as follows (rules depend on your Aliyah date): Nefesh B’Nefesh

- Aliyah before January 1, 2022: 3 points for the first 18 months, 2 points for the next 12 months, and 1 point for the next 12 months (3.5 years total).

- Aliyah on/after January 1, 2022: 1 point for the first 12 months, then 3 points for 18 months, then 2 points for 12 months, then 1 point for 12 months (4.5 years total).

These points reduce Israeli income tax on Israeli-source earnings, so they matter most once you are working in Israel.

What is a realistic 30-day setup plan that keeps you liquid and lowers fees?

A realistic plan is one that assumes delays and still keeps you funded: arrive with a small shekel buffer, open an Israeli bank account quickly, and move bigger money only after you have a tested transfer method. Use day-to-day card spending to minimize cash handling, and schedule one larger conversion instead of many small ones that each trigger fees.

What should you do in the first 72 hours after landing?

Focus on functionality, not optimization. Get a local SIM, withdraw a modest amount of shekels from an ATM using a low-fee card, and book your bank appointment. If you have benefits that require a bank account, prioritize opening the account even if the bank’s app feels clunky. Keep every receipt and document in one folder from day one.

What should be in place by day 30?

By day 30, aim for: an active Israeli current account, online access, a debit card, and one inbound transfer route you have tested end-to-end. You should also know your tax and reporting status. Once those basics work, you can optimize: negotiate bank FX rates, use a licensed dealer, or choose fintech for recurring transfers.

When is it worth paying a professional, and which professional?

Pay for help when one mistake costs more than the fee: property sales, six-figure transfers, business setup, or multi-country taxes. An Israeli tax advisor can clarify residency, exemptions, and reporting, and a home-country specialist can keep you compliant there. Use a mortgage broker or planner for big shekel decisions, not for routine transfers.

Bottom line

- Check the Bank of Israel benchmark rate first, then compare offers based on the spread, not the “commission.” Bank of Israel

- Use ATMs/cards for arrival-week liquidity, but watch foreign fees and always choose to be charged in shekels.

- For cash exchange, compare licensed changers and ask for the exact rate in writing. Government of Israel

- For large transfers, budget for the full wire cost stack: send fee, receive fee, and FX spread. Nefesh B’Nefesh

- Assume large transfers will trigger questions and prepare a source-of-funds folder before you move.

- Tax benefits are real, but 2026 disclosure rules and new incentives are date-dependent, so verify your status. Government of Israel

- Open your Israeli account early so benefits and salary payments do not get delayed. Government of Israel

Next step: open a notes file called “Israel Money Setup,” save your documents into one folder, and run one small test (ATM withdrawal or transfer) before you rely on it for a large move. One controlled test often saves weeks of frustration.

If you are planning to buy property in Israel, explore current homes for sale and our buyer guidance: browse Israeli homes for sale.

Thinking about your next move in Israeli real estate? Tell us what you are looking for and the Semerenko Group team will help.

Aliyah housing links for money-transfer planning

Currency timing is only one part of the move. Before transferring funds, connect the money plan to the property plan: the foreign-buyer guide, buying before Aliyah, the moving-to-Israel guide, and the rent-first framework for new olim.